Optimism is the regime; what we're underwriting is concentration and leverage.

The near-term backdrop has, for now, become more accommodating. A workable if fragile Iran–US framework has helped collapse 2026 rate-hike odds from roughly 80% to 40%, and the VIX has settled at 16.3. Should that durability hold and we'd stress the conditionality another tail risk leaves the table. Wednesday's FOMC is the next signpost; Warsh will calibrate the market's read on the path ahead. Our base case remains no hikes, and we'd reiterate a seasonal point worth respecting: April and May delivered the two best months for equities in the past decade.

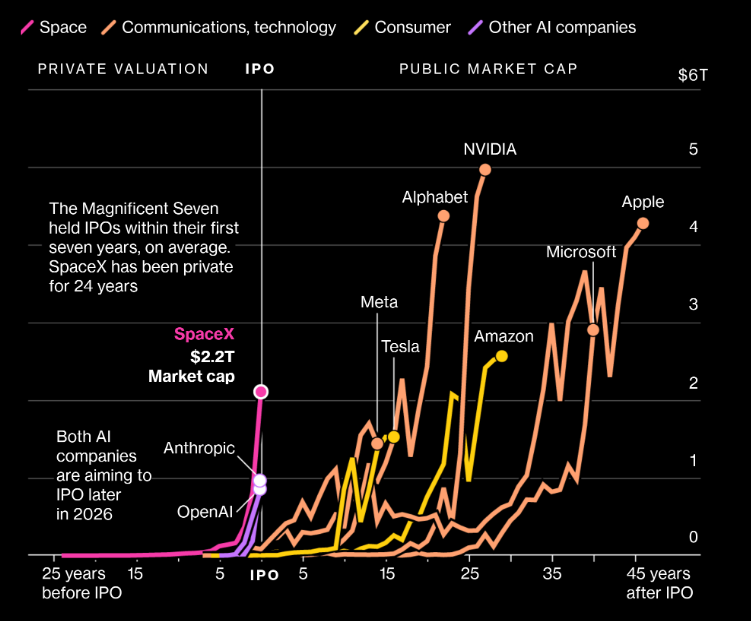

SpaceX dominates the tape. Up close to 45% to $212 in the largest IPO on record. We'd be candid about the thesis underpinning it: it is one of faith. Trying to reconcile that with a discounted cash flow is a category error, the same error one would have made pricing the railroads or the early web off the applications visible at the time. We don't dismiss the story. We simply observe that a market willing to capitalise faith is telling you something about where we are in the cycle.

Our central thesis is intact. This remains a narrow market carried by a single engine: the earnings trajectory of the AI spectrum. Q1 underscored it. The S&P compounded EPS at 25%, of which AI accounted for close to 60, versus a mere 14% from the entire remainder of the index. Beyond holding the line on valuations outside the US and the AI complex, we continue to find value in our Swiss and European quality-growth compounders across Luxury, Pharma, and Industrials.

The policy shock: frontier AI moves under state control

The more consequential development sat beneath the SpaceX noise, in Washington. A new export-control directive bars all foreign nationals, inside or outside the US and including Anthropic's own staff, from accessing Fable 5 and Mythos 5. The state is now gating models as it gates advanced silicon: frontier capability is strategic infrastructure, to be ringfenced as national defence. Two implications. First, a split between public and strategic AI, with the labs becoming hybrids, part consumer platform, part enterprise vendor, part defence contractor. Second, the end of open-borders AI talent, replaced by national champions, secured compute and supply chains, and an explicit US-China-rest contest in which the leading model is a sovereign asset.

What we're watching

Velocity is the defining variable. A month ago SpaceX ran no cloud whatsoever; today it plausibly operates the fourth-largest, having leapfrogged Oracle outright, a standing built in weeks rather than years. The public-private megacap boundary is dissolving on the same timeline: Anthropic and OpenAI now command $850bn–$1tn valuations, and SpaceX closed its first session sixth in the world. The reward for being positioned ahead of that is substantial, and Google's venture book is the cleanest illustration, SpaceX marked at roughly 140x ($0.9bn to ~$125bn), Anthropic at ~10.5x ($13bn to ~$135bn), Waymo at ~8.8x ($10bn to $88bn). It is the same balance-sheet mechanism that has just carried SoftBank to the top of the Japanese market through OpenAI and Arm.