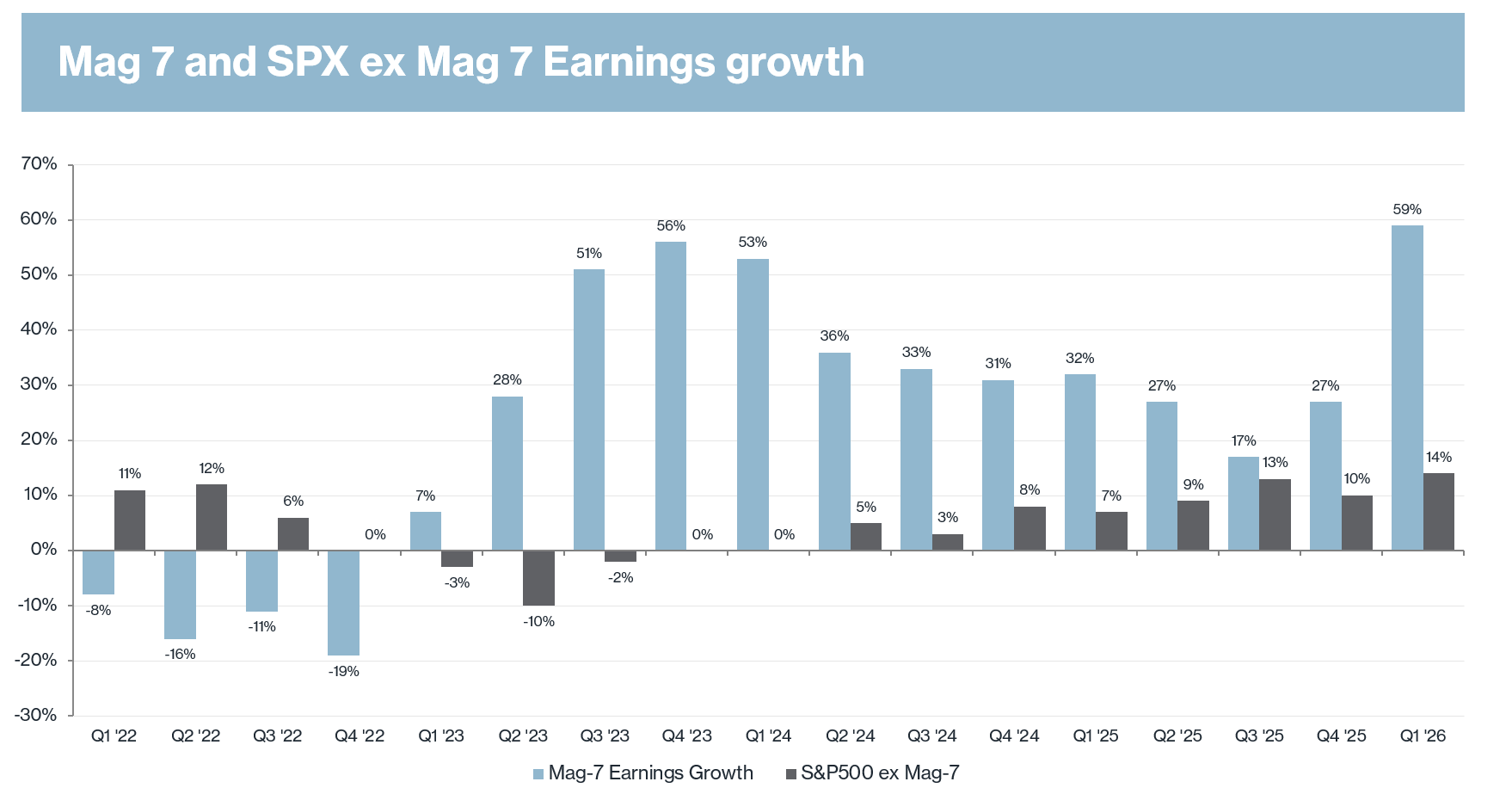

The big takeaway from last week is that US equities (Hard to ignore the Software move) just logged a ninth straight weekly gain, and while sceptics keep offering tidy explanations for the run frothy valuations, an over-optimistic read on the Iran situation, a sugar-high from fiscal spending, or funds being caught under positioned, the real fundamental reason are US Corporate Earnings, plain and simple – see below.

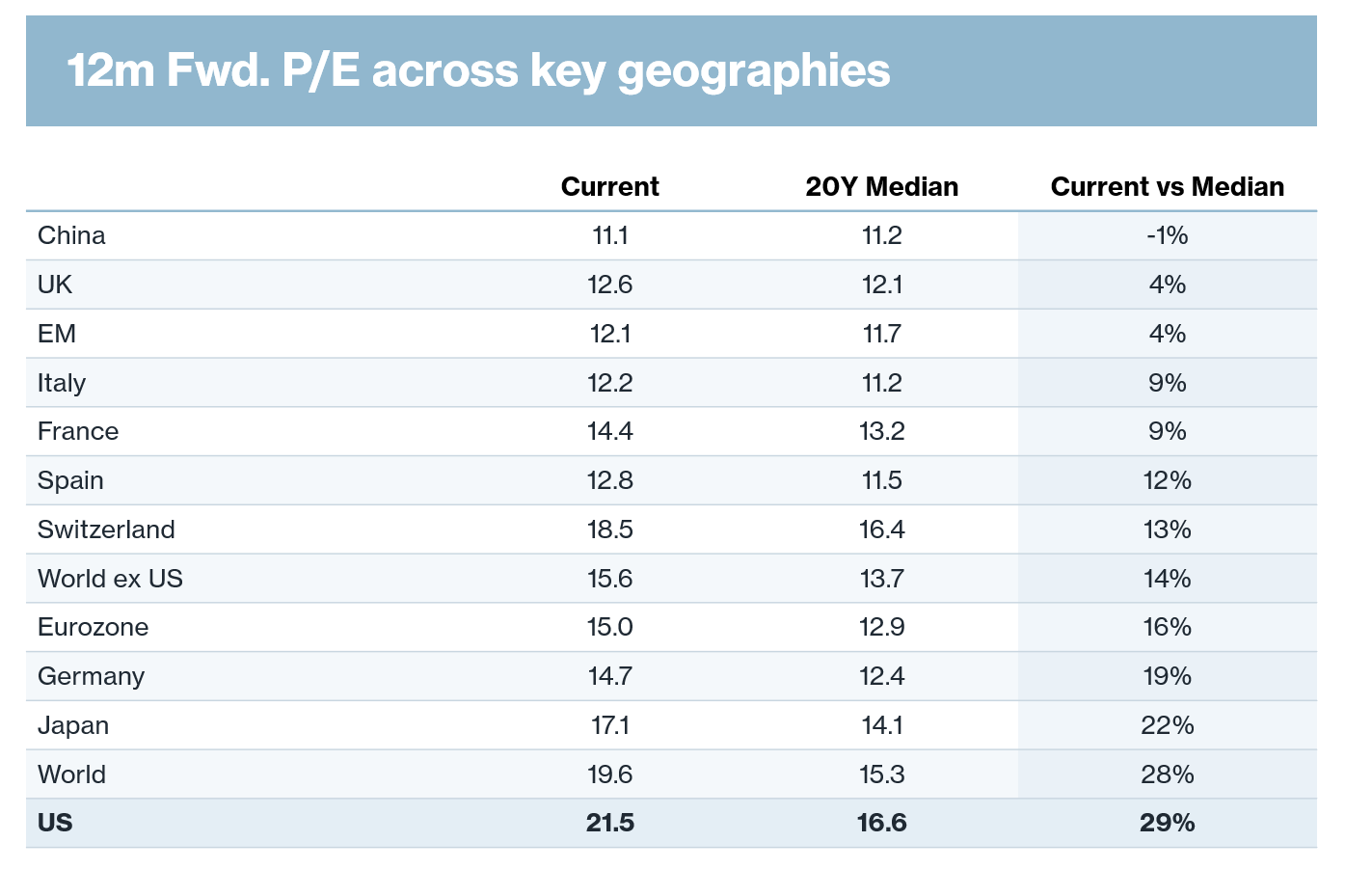

US earnings climbed 27% (largely driven by Tech &Energy) year-over-year last quarter, and although the S&P500 is up close to 11% on the year, valuations have slipped slightly (from 22x to 21x) while forward estimates have pushed higher. In other words, the gains have been earned rather than inflated by multiple expansion.

Looking forward, two cautions stand out: Positioning has grown stretched and speculative heavy call-option volume, surging leveraged-ETF assets, and it's an open question whether forecasters and companies can keep ratcheting earnings estimates up at this pace, even if double-digit growth (projected at 24% this year, 13% next, remember we came into this year with market estimates being at +12% for EPS growth 2026! ) should keep a floor under things as we are trading above long term P/E multiples.

The practical conclusion is to stay invested but continue to be disciplined on a single stock perspective since the easy market-cap gains of the past two months will be tough to repeat, and a momentum reversal heading into quieter summer trading is worth preparing for.